This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

At the TokenizeThis conference in New York this week, I had the pleasure of moderating a conversation with executives from Dinari and STOKR on the potential for tokenized stocks.

I also caught a panel on the retail adoption of tokenized real-world assets (RWAs) more broadly. The headwinds, tailwinds, what have you.

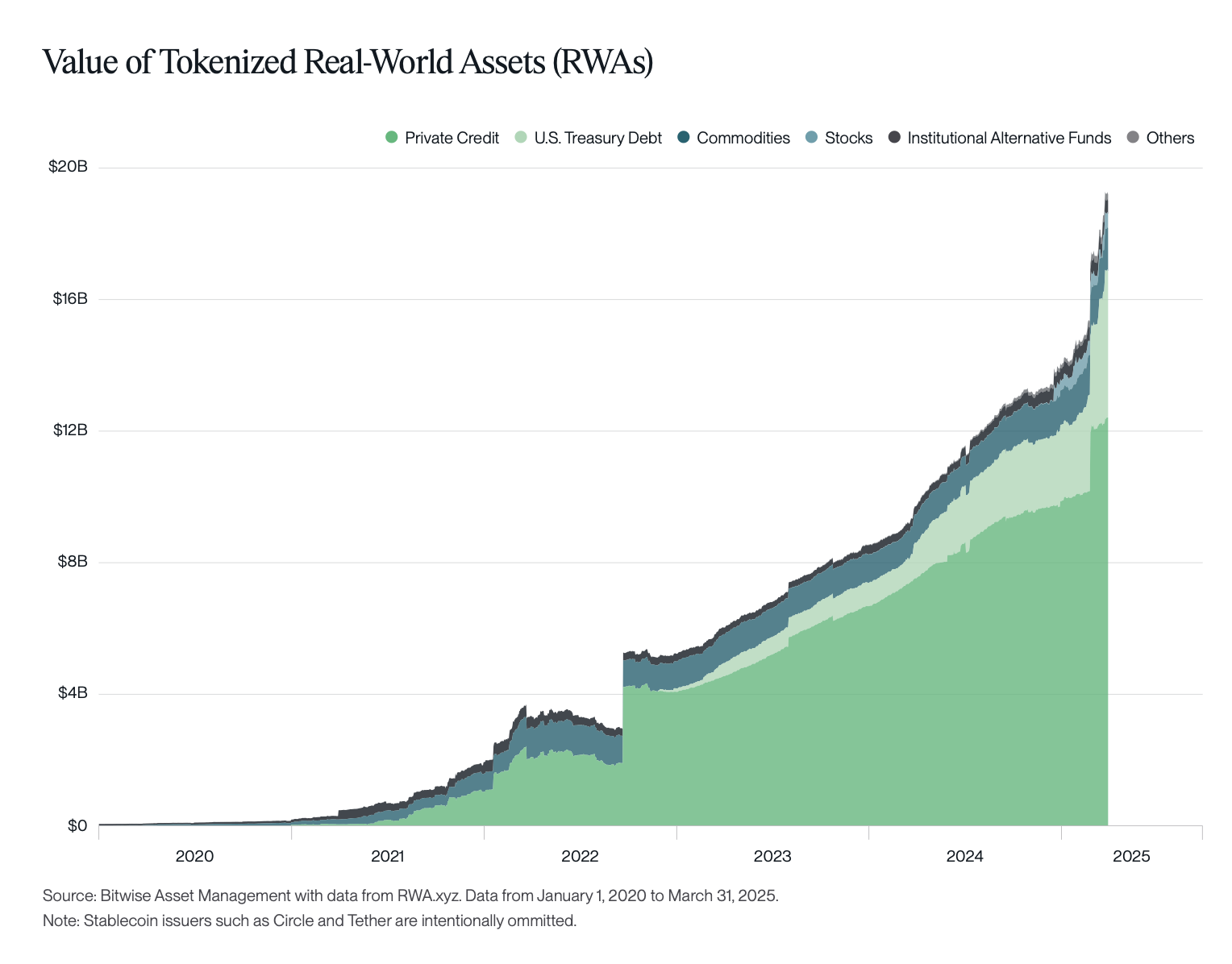

First things first: Stablecoins (primarily tokenized dollars, so to speak) are a nearly $230 billion market. Outside of that, onchain RWAs currently amount to $18.5 billion, RWA.xyz data shows.

A recent report from Bitwise called Q1 “the best worst quarter in crypto’s history.” While asset prices fell, stablecoin market cap hit a new high and tokenized RWAs grew 37% quarter over quarter. Not to mention regulatory progress.

Source: Bitwise

You can see that big chunk in private credit, and the other substantial piece in the US Treasury debt category. Included in that is BlackRock’s tokenized money market fund, BUIDL, which recently hit the $2 billion Assets Under Management (AUM) mark.

Expected legislation in the US that “allows on-ramps and off-ramps to proliferate” will be crucial, Neoclassic Capital managing partner Mike Bucella said on the TokenizeThis stage Wednesday. Stablecoins and tokenized Treasury products will thus be “the foundation” for more creative onchain offerings in the coming years.

“The boring stuff is an absolute necessity, because it exists in the offchain world,” he explained. “If you can’t do that in the onchain world, then you’re not going to sit there and wait for some interesting onchain yield product; you’re going to go offchain into the traditional markets.”

As for where we go from here, Dinari Chief Business Officer Anna Wroblewska argued that after stablecoins and money market funds, publicly listed US stocks offer another easy access point for investors looking to move onchain.

Galaxy Digital tokenization head Thomas Cowan, however, noted the already-solid user experience to invest in stocks on venues like Robinhood. Therefore, he asserted, the next wave of growth could come in “places where there’s a clear lack of transparency [and] settlement risk” — i.e. private credit.

Sitting beside Cowan, 21Shares US sales head Anton Kozlov added that he also sees demand for tokenized private equity — pointing to SpaceX and OpenAI. Blockworks Research analyst Carlos Gonzalez Campo expects shares of such private companies to be tokenized within the next four years.

Crypto custody firm Taurus, in a recent report, pegged the “market opportunity” of fund tokenization at $1 trillion by 2030. While money market funds unlock use cases in collateral management, the report notes, Taurus is also bullish on tokenization within illiquid segments.